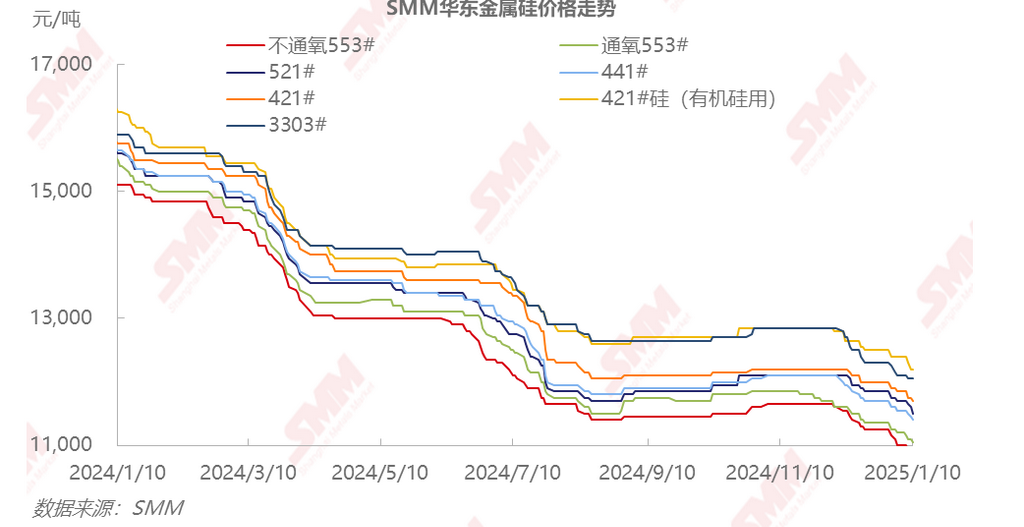

SMM, January 12: Spot silicon metal prices continued to decline from December to early January, with a wider drop compared to the previous month. As of January 10, above-standard #553 silicon metal in east China was priced at 11,000-11,100 yuan/mt, down 550 yuan/mt MoM; #441 silicon metal was at 11,300-11,500 yuan/mt, down 550 yuan/mt MoM; and #3303 silicon metal was at 12,000-12,100 yuan/mt, down 650 yuan/mt MoM. In the futures market, the most-traded Si2502 futures contract continued to fall, hitting a low below 10,400 yuan/mt. Based on quotes from suppliers, silicon enterprises, and futures-spot traders, the low futures prices have led to significantly lower prices for traders' supplies compared to those of silicon enterprises, making order signing difficult for silicon enterprises. However, considering the limited downstream demand and the support from production costs, silicon enterprises are reluctant to offer significant discounts in the short term. The market remains active in futures-spot transactions.

Supply: According to SMM data, China's silicon metal production in December was 331,600 mt, down 73,100 mt or 18.1% MoM, and down 5.2% YoY. Production in Xinjiang, Yunnan, and Sichuan all saw varying degrees of decline. The operating rate in Xinjiang dropped mainly due to maintenance of some capacity by top-tier enterprises in December, with the shutdowns significantly impacting the month's production. In January, top-tier enterprises in Xinjiang are expected to further expand production cuts, leading to a further decline in operating rates. The number of operating silicon enterprises in Yunnan and Sichuan continues to decrease, with production expected to decline further. China's silicon metal production in January 2025 is expected to drop to around 300,000 mt, with operating rates remaining weak.

Demand: According to SMM data, polysilicon production in December was 93,100 mt, down 17% MoM. Polysilicon enterprises showed weak operating rates before the Chinese New Year, and polysilicon producers are expected to maintain operating levels during the holiday. Post-holiday, operating rates are expected to increase in March, with further demand growth for silicon metal anticipated in Q2. Actual operating conditions need to be closely monitored. For silicone, SMM data shows December DMC production at 227,000 mt, up 3% MoM. January silicone production schedules are expected to slightly adjust to below 220,000 mt. In the primary aluminum-silicon alloy sector, December operating rates fell by about 1 percentage point MoM, while the secondary aluminum-silicon alloy sector also saw a 1 percentage point MoM decline, with limited impact on silicon metal consumption.

Bullish Factors: Expanded production cuts on the supply side

Bearish Factors: Time needed for downstream operating rate recovery; funding needs of some suppliers

SMM Viewpoint: Overall, based on supply-demand balance calculations, the silicon supply surplus in December was around 20,000 mt. In January, both supply and demand for silicon metal are expected to remain weak, with a roughly balanced supply-demand performance. Due to the larger-than-expected decline in January silicon metal futures prices, futures-spot transactions were moderate, and some social inventories were transferred. However, overall industry inventory has not been effectively destocked. Downstream users have mostly completed stockpiling before the Chinese New Year. Given the long time frame, the large number of suppliers, and low prices, pre-holiday restocking sentiment is not strong. Some small and medium-sized silicon enterprises in northern regions plan production cuts after the holiday due to pressure from losses. Meanwhile, new capacity is gradually entering the market. Attention should be paid to changes in operating rates of small and medium-sized silicon enterprises on the supply side and operating rates in the downstream polysilicon sector before and after the Chinese New Year.

For more detailed market information and dynamics, or other inquiries, please call 021-51666820.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)